Commodity markets remain soft as recession fears linger

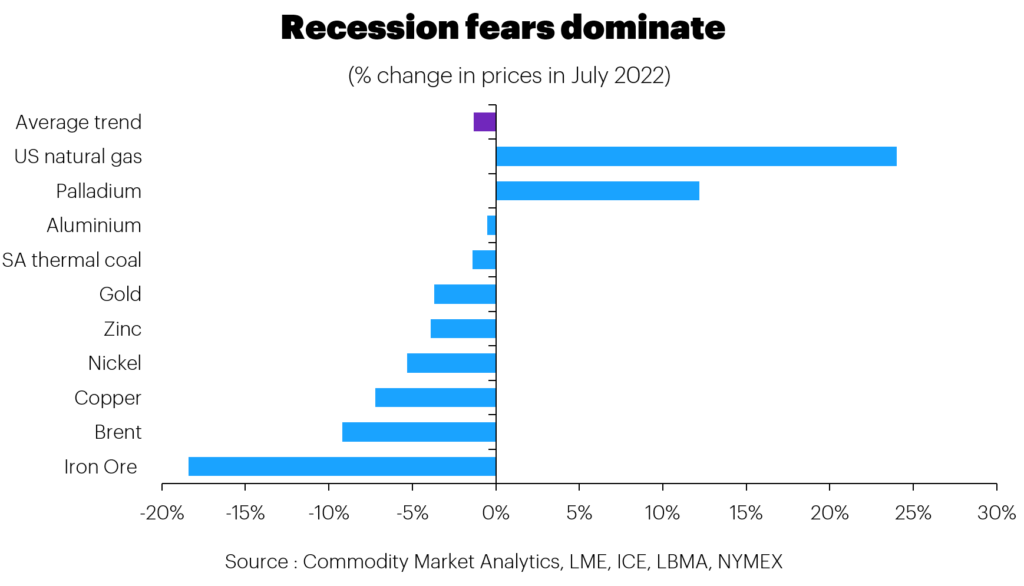

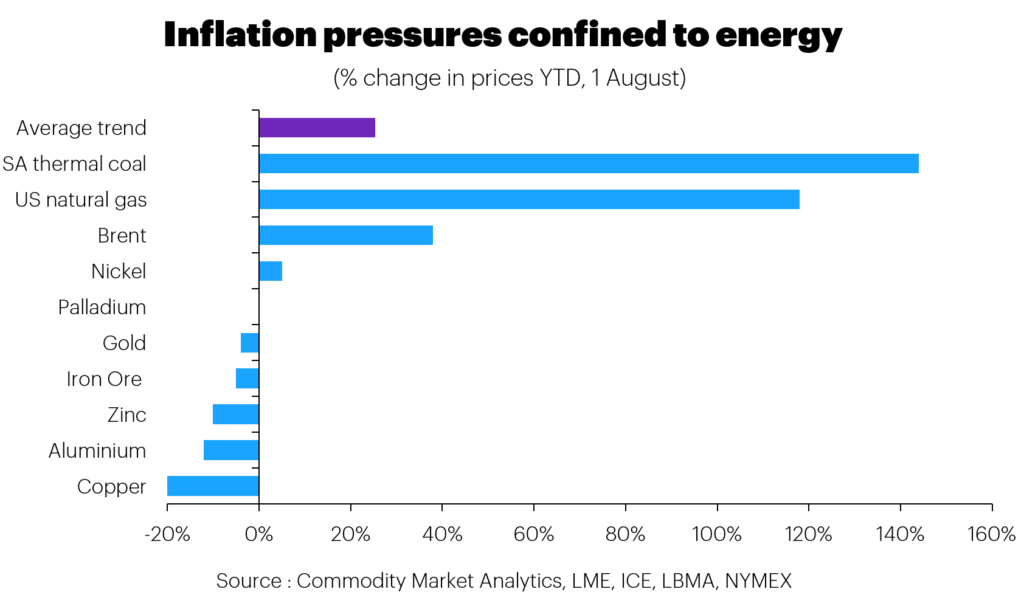

The past month has seen bearish sentiment continuing to weigh on commodity markets as inflation remains strong and China is yet to accelerate out of its Covid-induced slump convincingly. Brent oil fell by 9% m/m (28 July), copper dropped by 7% m/m, and iron ore tumbled by 18% m/m, reflecting ongoing weakness in the steel market.

Macroeconomic factors continue to drive commodity markets.

In July, the 4% drop in the Shanghai equity index highlighted how government stimulus measures have not yet been enough to turn sentiment around in China, a key consuming country for steel and base metals. GDP growth in the country was just 0.4% y/y in Q2, as strict lockdowns resulted in sharp falls in manufacturing activity. Moreover, the official composite PMI fell to 52.5 in July, from 54.1 in June.

Meanwhile, in the US, the headline economic data also looks soft, with GDP falling by an annualised 0.9% in Q2. Markets are, however, looking beyond this and are trying to anticipate when US interest rates will peak, as this would mark a turning point for risk appetite.

In terms of fundamentals, the oil market is starting to soften once more because Russian oil production has been resilient in the face of sanctions. Global demand growth is beginning to slow in line with weaker manufacturing activity and high oil prices.

The IEA estimates that the oil market was in surplus in Q2 and will remain in surplus in the second half of this year. Oil demand is forecast to rise by 1.8% this year, but oil supply will increase by a hefty 5.1%, reflecting an unwinding of previous emergency cutbacks by OPEC. Russian production is predicted to drop by 0.3mb/day this year, but this will be more than offset by Saudi Arabia, which will increase by 1.6mb/day, while other members of the OPEC group will raise output by 0.9mb/day. However, inventory levels remain extremely low, so any supply setbacks would quickly feed through to higher prices.

Copper also had a poor July, but prices started to pick up late in the month in response to tight fundamentals and a lack of available LME stock. Company results highlighted ongoing challenges on the supply side of the industry. First, Glencore cuts its full-year guidance for copper output by 5%. Output fell by 15% in the first half of this year due to problems at Katanga in the DRC and Collahuasi in Chile.

Furthermore, MMG reported a 52% drop in copper production in Q2 due to problems at Las Bambas in Peru, where protestors have halted operations. However, output at Russia’s Nornickel rose by 18% in H1, despite sanctions and this provided some offset to weakness elsewhere.

Reduced supply has meant that the global trend has been towards a tighter copper concentrate market, with spot treatment charges (TC) trending down in July. Spot TCs were above USD80/tonne in early May but fell to USD68/tonne by the end of July, according to Fastmarkets. This is a bullish development for the copper market.

However, a weak steel market highlights soft demand for industrial metals more generally, helping to drag down iron ore prices. In the first six months of this year global crude steel production fell by 5.5% y/y, according to World Steel Association data, with June down 5.9% y/y. Problems in China have played a big part in this, with a 6.5% fall in H1.

Looking ahead, the downside for metal markets is becoming limited, with China set to accelerate out of its recent slump. Base metals will be supported by this as well as exceptionally low levels of inventory. Energy prices look set to remain high and volatile ahead of the northern hemisphere winter.

Expectations for global demand are likely to turn higher soon, leaving commodity markets vulnerable to another price spike.