Commodity markets rally as the world economy pulls out of its slump

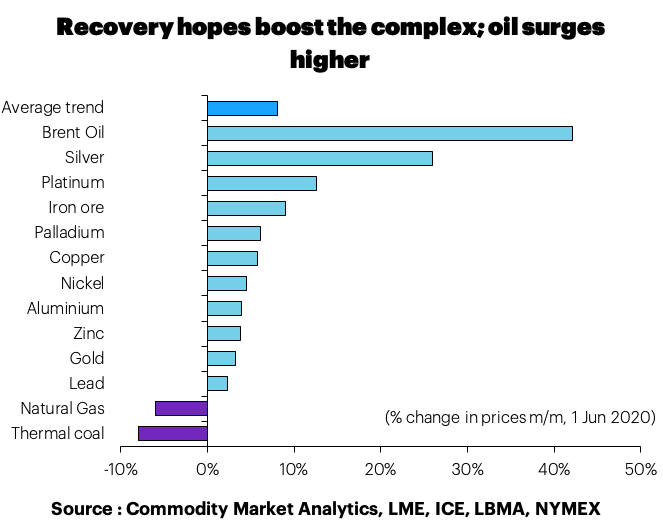

May saw bullish sentiment sweep through the commodities complex, with nearly all major markets rallying.

Oil led the way higher with a 42% jump, iron ore rallied by 9%, and the base metals increased by 2-6% m/m. Demand is improving rapidly for many commodities, but from a very low level and oil producers are cutting aggressively.

Many financial markets have rallied strongly, and indicators of risk appetite are flashing green, despite the fragility of the current economic recovery. For example, equity bulls are outnumbering bears, with the market focussed on the prospects for recovery, rather than worrying too much for now about the chances of another virus-related slump.

The S&P 500 is up 8% m/m (as of 1 June), the FTSE100 is up 6% m/m, and the Shanghai Composite is up 2% m/m, despite concerns about political developments in Hong Kong. Ample liquidity from the world’s central banks and promises of fiscal stimulus are helping to offset more immediate challenges on the economic and political front.

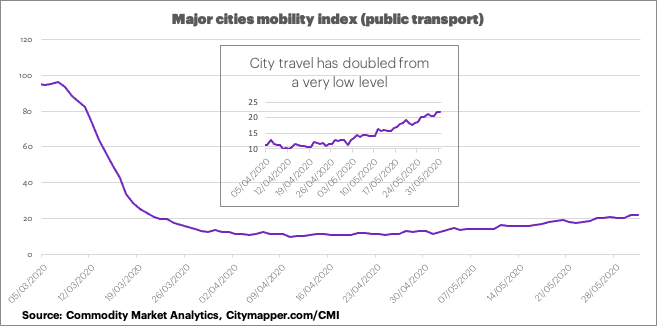

City travel has more than doubled from its recent low point

The steady easing of lockdowns in Europe and the US has reinforced the idea that the worst is over for global economic growth.

Data from Citymapper shows that travel by public transport in the world’s largest cities has more than doubled from its recent low point, although it is still dramatically down on normal levels. The index fell to a low point of 10.1 on 10 April but rose to 21.7 by the end of May. This data would look notably stronger if China were included.

The recovery underway is a fragile one and depends on politics and virus control

However, this optimism could quickly be shot down by fresh problems, and there are two key elements to monitor as we move into the early part of a recovery phase.

1. Will the virus outbreak explode into a second wave?

Here the US seems to be at particular risk, given the high levels of infection and the political unrest that is currently flaring up around race relations. The US currently has more than 1m people infected by the coronavirus, and the number of new cases being registered is still stubbornly high.

2. Will the US President escalate his trade war with China?

Tensions could have increased recently due to threat to Hong Kong from an imposition of new stricter Chinese laws that appears to threaten the “One country, Two systems” approach.

But for now, the risk of another spat in the ongoing trade war appears to be low, as the President is forced to focus on domestic issues. The Phase One trade deal painfully agreed between China and the US looks safe for now, and this should help the recovery going forward.

PMI figures for China, Europe and the US point to a brighter future

The most recent global PMI data helps to support the mildly bullish narrative. The Chinese services PMI rose from 53.2 in April to 53.6 in May.

Also crucial for the mining sector was the sharp upturn in construction indicators in the country. This subcomponent rose from 59.7 in April to 60.8 in May and orders have accelerated recently, pointing to a strong second half of 2020.

This is good news for steel, copper, zinc and other construction-related markets. One reason for the upturn is that the Chinese government recently announced additional stimulus measures for the economy. According to Reuters, these account for 4% of GDP – the most significant stimulus since the global financial crisis.

Typically, the construction/infrastructure markets get a boost from these measures. Furthermore, the European manufacturing PMI rose from 33.4 in April to 39.4 in May, while the US moved from 41.5 in April to 43.1 in May, marking another slow move back towards normality.

Oil prices have recovered from a near-death experience, as producers cut like crazy

The roller coaster ride for oil prices continued this month, with Brent oil prices up 42% m/m, but still down 43% from the start of this year at USD37pb. Demand has been lifted by increased travel in many parts of the world, but more important is that oil producers have been aggressively cutting supply.

The OPEC+ cartel has led the way, with a massive 10mb/day cut for May and this has been maintained for June and might even be extended into H2 2020, according to the latest newsflow. Moreover, compliance with this latest cutback plan has been surprisingly high, with even Russia helping in a meaningful way. Oil prices have been so low recently that margins have been crushed for nearly all producers and so the cuts extend well beyond the cartel.

We’ve seen significant retrenchment in places like Canada and the US, where output is slumping. Output in Canada was down by 13% y/y in April, and the US is down 5% from its recent peak. The problem for oil is that spare capacity is now huge, and inventory levels are bloated. This means that oil prices are likely to remain depressed for the foreseeable future.