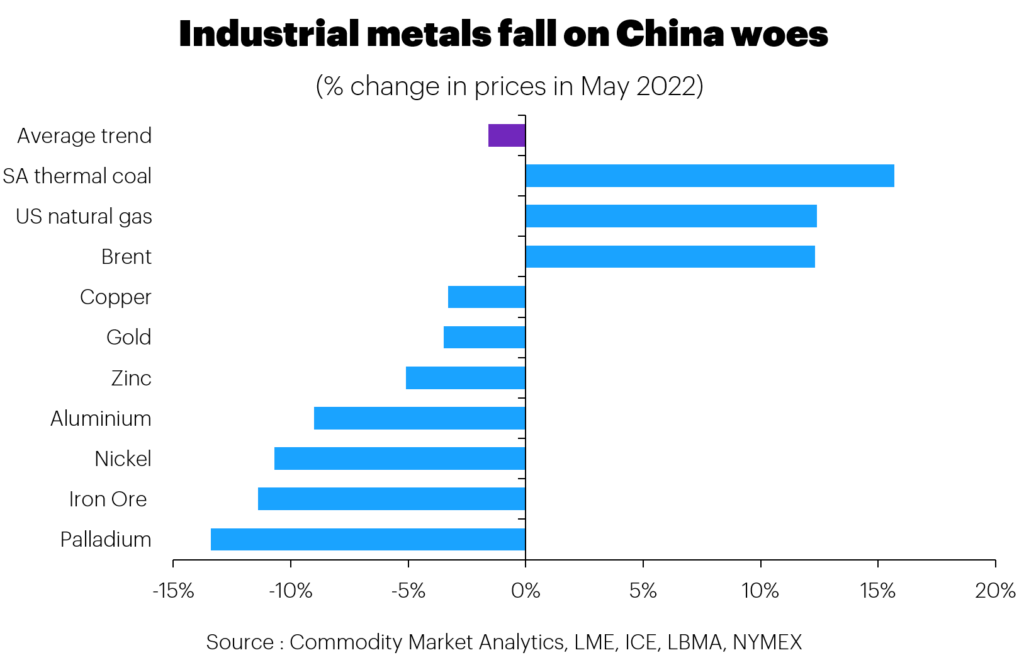

The past month has seen significant divergence emerge across the commodities complex, with energy prices continuing to push higher while industrial metals have fallen.

Brent oil is up 12% m/m (as of 31 May 2022), while US natural gas is up 13%, and thermal coal is up 16% m/m.

By contrast, aluminium is down 9% m/m, while copper is down 3% m/m. This year, most of these markets have seen wild swings as the war in Europe disrupted supply chains and consumers rushed to lock in raw materials.

However, many industrial metals have seen sharp falls in recent months, and prices are not too far from where they were at the start of this year, despite the backdrop of very elevated energy prices. Aluminium is down 1% so far this year, while copper is down 3%.

Aluminium prices briefly surged above USD 4,000/t in early March, after the Russian invasion of Ukraine, but since then have dropped by around 30%. The lacklustre price performance is particularly surprising given that it is a very energy-intensive metal to produce – around 40% of operating costs are energy-related. Also, Russia is an important producer, with 6% of global output.

So, what has happened to bullish sentiment?

The biggest problem is that demand in China is looking very weak, creating significant headwinds. The economic data for April looked extremely poor, and May will probably not be much better due to strict lockdown measures being imposed in places like Beijing and Shanghai to contain Covid outbreaks.

The manufacturing sector in China is struggling and key sectors such as automotive and construction saw activity tumble. Car sales were down by 46% y/y in April, and housing starts were down by a similar amount. In mid-May, 187 million people in thirty cities in the country were still under full or partial lockdown measures.

The weakness in Chinese aluminium demand is illustrated nicely by the trade data. In April, imports were down by 38% y/y, while exports of aluminium and aluminium products rose 37%. The country has switched from being a significant net importer to an exporter, which is very unusual.

The global alumina market also looks to be oversupplied, helping to ease cost pressures for aluminium producers. Prices were above USD500/t in mid-March, but since then have fallen back to USD360/t by the end of May. Australia announced a ban on alumina shipments to Russia, which has diverted more material into the spot market, with many consumers already well-stocked.

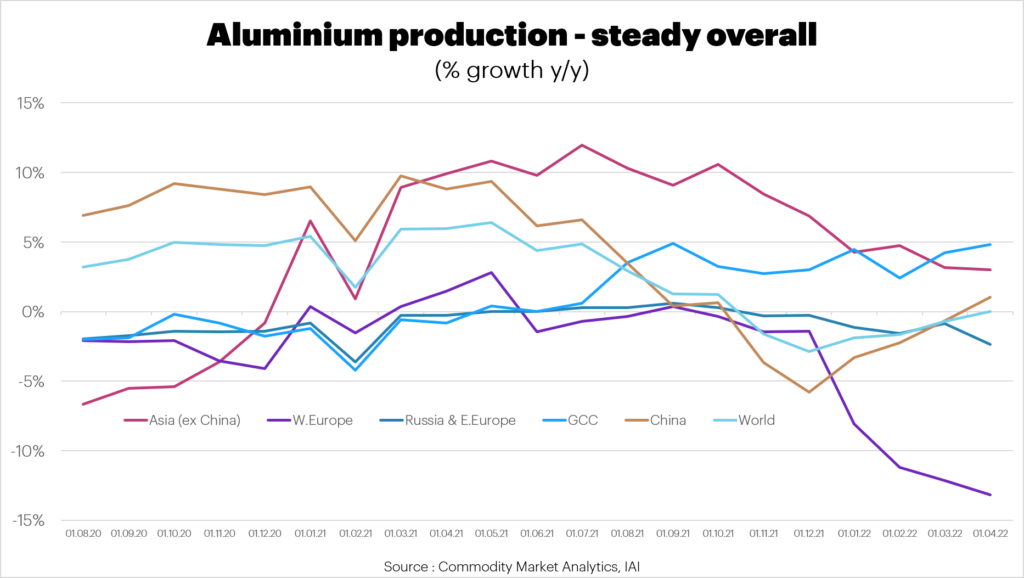

Finally, looking at aluminium production, this has been steady, despite the challenges discussed above. Global aluminium production was unchanged y/y in April, as we show below.

While there were cutbacks in places like Europe, North America, and Russia, these were exactly offset by growth in Asia and the Middle East. Fears about supply shortages appear to be misplaced.

Oddly though, on-warrant LME inventory levels are in sharp decline. These were down by 50% in May, suggesting that the market is in deficit. However, it seems more likely that this decline is the result of metal being moved outside the official reporting system for storage rather than consumption.

It is a warning signal that bearish sentiment should not be overdone.

Aluminium is an interesting case study of how markets are coping surprisingly well so far with the challenges of rising inflation and threats to supply chains in Europe. Panic buying saw prices jump in March, but demand weakness has dampened bullish sentiment.

Looking ahead, we expect a strong rebound in economic activity in China soon as the government chases its target of 5.5% GDP growth for the year. This will tighten the base metal markets and create upside risks for aluminium, particularly if energy prices remain elevated.