Commodities and Covid trends reflect a divided world

October saw a return to volatile trading conditions in commodities and the world’s largest financial markets more generally. Equity markets tumbled in Europe, as a second wave of Covid-19 infections caused fresh alarm.

Many countries in the region, including France, Germany, Italy, Spain, and the UK were forced to severely tighten lockdown measures, such as closing bars, restaurants and non-essential shops and restricting travel. The US is also suffering with very high infection rates.

By contrast, Asian and Chinese equity markets trended up, and many Asian countries are operating more normally, with infection levels extremely low in China. Australia is lifting its restrictions.

Inevitably progress with tackling Covid will drive the economic story in the months ahead, but the latest data is already indicating a slowdown, even ahead of the latest lockdowns.

Flash PMI survey data for the world’s four largest developed economies (Eurozone, Japan, the UK, and the US) showed that activity was at 51.9 in October, down from 52.0 in September. Within this total, the service sector is slowing, hiring activity is cooling, and growth in new orders is stuttering. In contrast, in China the Caixin manufacturing PMI showed an acceleration to 53.6 in October, up from 53.0 in September.

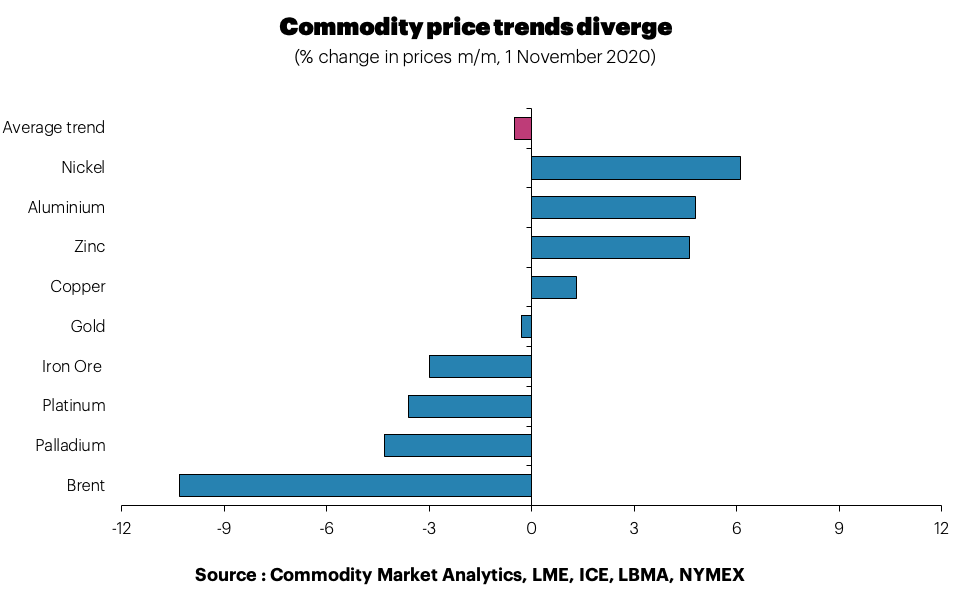

In October, commodity price trends also reflected this divided world of Western weakness and Asian strength. The base metals managed to rally, despite the troubled backdrop, with aluminium, nickel and zinc all making decent gains, helped by an optimistic view on China.

Meanwhile, Brent prices tumbled below USD40pb, on reduced expectations for travel and as OPEC moderated its previous output cuts. Finally, gold was barely changed for the month, as it struggled to make any gains against a backdrop of USD strength.

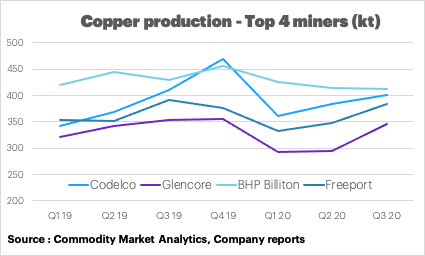

Covid is also impacting the supply side though for miners, which is helping to support the bullish argument for base metals. Third-quarter results from the four largest copper mining companies – BHP Billiton, Codelco, Freeport-McMoRan and Glencore – are shown in our table below. The results showed significant weakness in recent quarters. However, after a 4.4% drop in Q2 2020, production was down a more modest 2.6% in Q3, as some mines restarted, and workforce numbers slowly increased. Clearly, there has been a significant impact from the virus, which is creating some tightness in the raw material markets, and this is taking some time to overcome

Glencore reported a modest 1.8% y/y drop in copper output in Q3, making it the least impacted of the large producers. One reason for the cutback was that Mutanda (DRC) was placed on care and maintenance back in November 2019, due to low cobalt prices. Also, the Antamina mine (Peru) saw a temporary suspension in Q2 2020, to tackle Covid infections. These falls were only partly offset by increases at Collahuasi (Chile), after operational improvements, and Katanga (DRC). The worst appears to be over though for the company, as output increased from 295kt in Q2 to 347kt in Q3.

BHP’s copper production has also been hit. Output was down by 4% y/y in Q3, making it the most impacted of the large producers. One problem was that its operational workforce in Chile was down by 30% in the most recent quarter, due to the virus. We’ve also seen significant falls in output in Peru. These falls were partly offset by a large jump at Olympic Dam in Australia, helped by productivity improvements.

Finally, Chile’s Codelco was down just 0.1% in August, following on from a 4.4% drop in July. The main challenges were at El Teniente, where sharp output falls more than offset increases at other mines such as Andina, Chuquicamata, Radomiro Tomic and Ministro Hales. Based on the first two months of the quarter, the company is on track to fall by 2.1% y/y in Q3.

In summary, October turned out to be another troubled month for the commodities complex, as rising Covid infections in Europe led to another round of lockdowns, denting demand in a key region.

Meanwhile, the Covid impact on Latin America is still significant, but easing. By contrast, China is still barrelling along in terms of demand, as its virus situation looks under control, and the economy is growing well.

Commodity markets are likely to remain very volatile in the months ahead, as bearish investor sentiment in the West collides with the bullish pull of Chinese physical demand. Downside risks still look elevated for markets like copper and gold, although oil is probably not too far from a floor, given that prices look unsustainably low for many US producers and OPEC is starting to get nervous once more.

Dan Smith, Director – Special Projects