Commodities markets rally, but oil looks overextended

There was a widespread rally across the commodity markets in the first two months of this year, as bullish tailwinds swept through many financial markets.

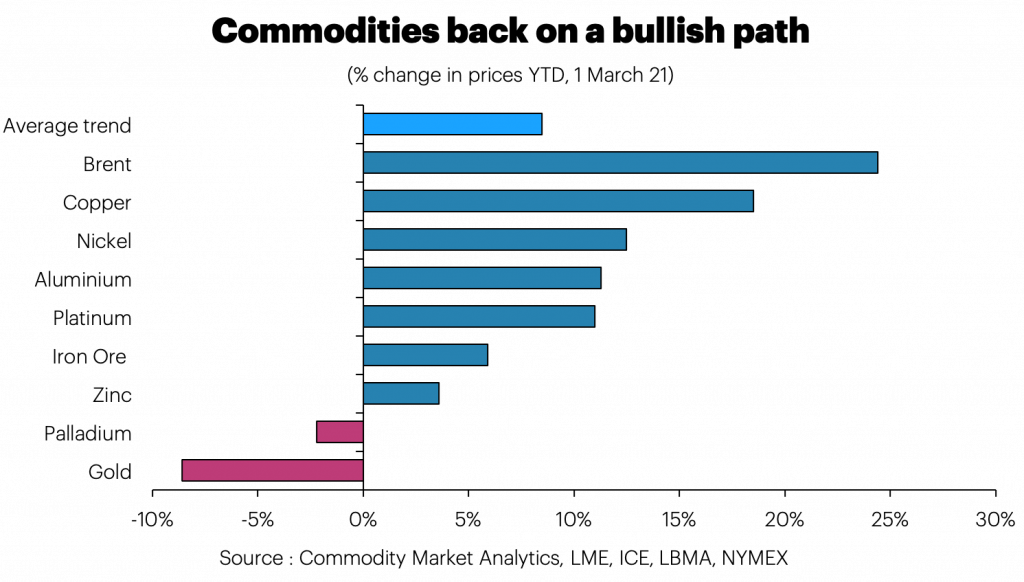

Brent was up 24%, copper up 19% and nickel 13%. Major drivers of the rally were rising inflation, a weaker USD and an expectation that this year will see a strong bounce back in economic activity, as Covid-problems recede and central banks and governments press hard on the accelerator.

Oil also got a boost from severe winter weather, which hit key producers in Texas.

Gold was a notable exception; prices fell by 9%, reflecting a reversal of safe-haven buying.

Surprisingly, fundamentals do not seem to be counting for much on the face of it, and the rally in oil seems more difficult to justify from a long-term perspective. Oil is now up by 240% from its low point in April 2020, while copper is up by a relatively modest 84%.

However, oil’s fundamental position is weak – surplus inventory is high, spare capacity is ample and demand globally is still very depressed compared to the high-water mark of 2019. Despite this, prices have bounced aggressively.

Copper, on the other hand, looks very well positioned from a fundamental perspective. Demand grew modestly in 2020 and should develop well over the next few years. Meanwhile, the industry’s mining side is struggling to keep up with smelter demand. As a result, treatment charges have fallen to very low levels at the start of 2021. Finally, the green energy revolution should spur an acceleration in demand over the medium term.

However, it is crucial to recognise that we cannot ignore valuations, and the starting point for the recent rally in prices is important. Oil prices have bounced back from extremely low levels, and copper is rallying from a relatively high starting point, which helps explain why copper has fallen behind recently. Prices today are probably not too far from fair-value in both cases, although we still believe that copper has the greater potential than oil to spring an upside surprise over the next few years.

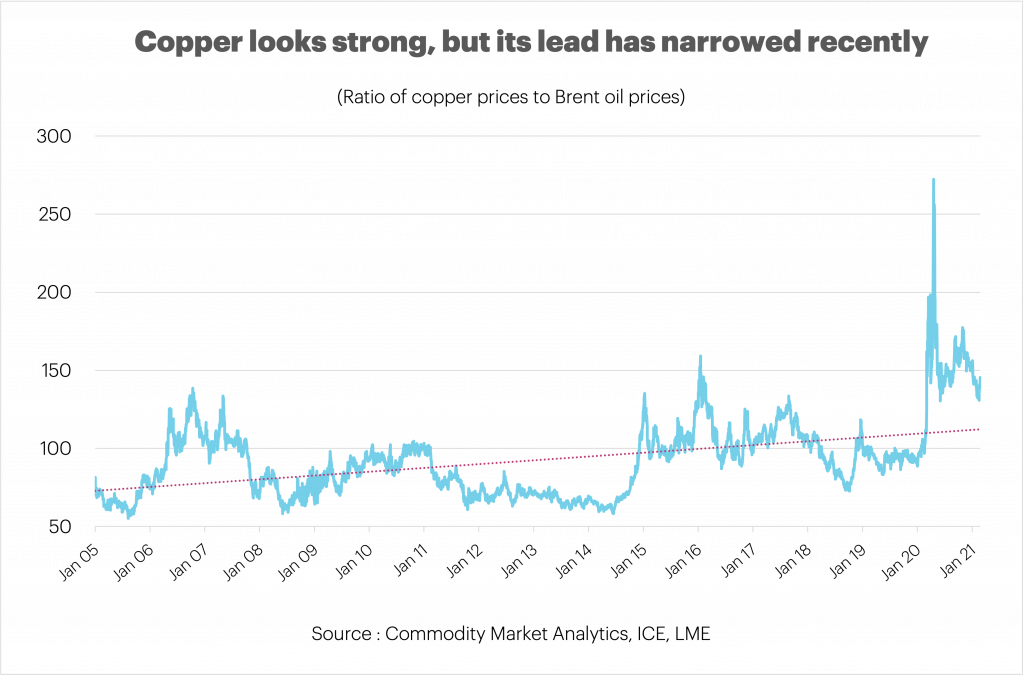

Copper looks strong but its lead has narrowed

Looking at the long-term relationship between oil and copper provides an interesting insight into the potential risks (see below).

We divide copper prices by oil prices to ascertain how the two markets have been moving relative to each other. This ratio removes common elements that drive all commodities, such as Covid-19, global economic growth and the impact of investors and the USD.

We can see from the dotted long-term trend-line that the ratio has risen from around 70 at the start of 2005 to about 115 by February 2021. Copper has been outperforming oil and has tended to rise more quickly in the good times and fall back less in the bad. However, the past year has been something of an aberration. Oil has been stronger, with the ratio falling from a peak of 272 in April 2020 to 145 by the end of February 2021. Partly this is because oil was so cheap back in early 2020, but we can see that this relative strength is a rare occurrence.

We expect the long-term trend to reassert itself soon. Copper should start to outperform oil once more, as its superior fundamentals become more apparent and the world moves past its Covid-related bounceback. While a rising tide tends to lift all boats, fundamentals will dictate the journey ahead.

Dan Smith, Director – Special Projects