China wants lower commodity prices, but it faces a dilemma

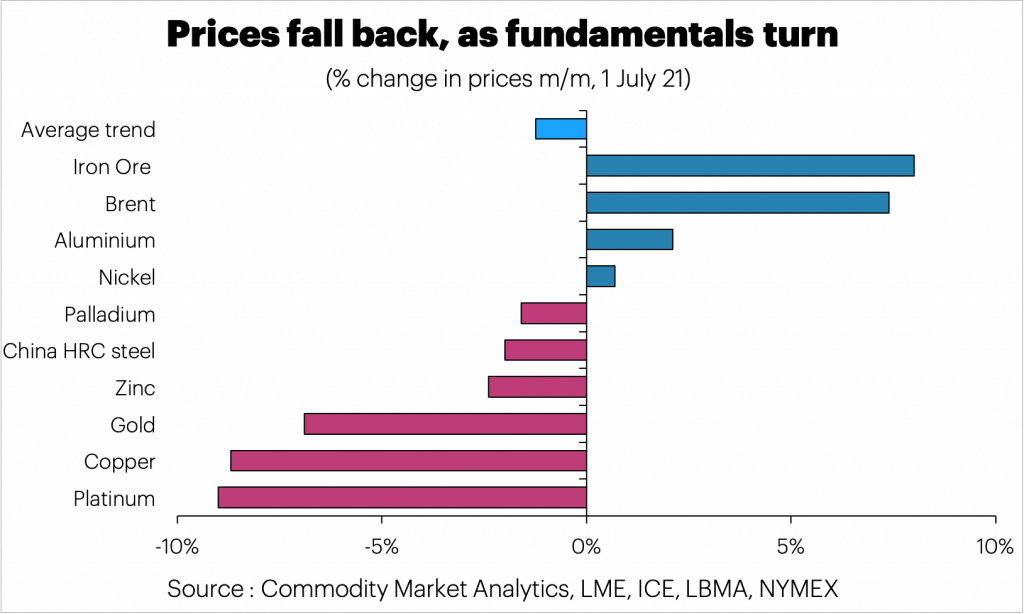

Recent weeks have seen a change in behaviour in the commodity markets, with many industrial markets falling, despite a decent economic backdrop and continued increases in global equity markets.

While crude oil and iron ore prices have continued to rally, we saw significant falls in copper, gold, the platinum group metals, Chinese steel and zinc.

Bearish drivers included reduced investor fears about inflation, a stronger USD, and weak Chinese demand, critical for many industrial metal markets. Chinese metals demand growth currently looks lacklustre. Local inventory is building, reflecting complaints from domestic consumers about high prices.

According to Fastmarkets, bonded warehouse stocks for copper were up 4% in June and copper premiums were close to five-year lows at the end of the month. Imports of copper also fell from 484kt in April to 446kt in May, which backed up the idea of moderate growth.

Chinese steel profits are also in decline, highlighting the difficulty of passing through high iron ore prices. Rebar margins were down from USD149/t in May to USD30/t in June, and HRC margins were down from USD155/t in May to USD62/t in June.

Finally, the Caixin PMI data for Chinese manufacturing confirmed an easing of activity, with the index falling from 52 in May to 51.3 in June.

The Chinese government would certainly like to see lower raw material prices to help domestic manufacturing.

However, it is facing a significant conflict between ESG concerns (which suggest a move towards burning less coal and reducing the production of industrial metals) and a desire for lower prices (which means ramping up production).

There is no doubt that climate change is a major concern for the country. China has many important coastal cities (including Shanghai) and is forecast to be the country that will be impacted most by rising sea levels.

For now, the environmental lobby appears to be losing ground, with steel production still up by a robust 14% y/y in the first five months of 2021, despite talk of production cuts.

China has started to pull the trigger on sales of strategic metal reserves for the base metals, although this looks like a short-term sticking plaster for a long-term problem.

In mid-June, sales of 20kt of copper, 50kt of aluminium and 30kt of zinc were announced. This helped to bring down prices in all three cases.

Copper looks most vulnerable to further significant selling in the months ahead, given that the country stockpiled around 500kt of metal last year.

However, a structural shortage of metal can only be tackled by matching supply and demand, which could prove to be a significant challenge in the years ahead if the green energy transition accelerates as expected.

China needs to find a better way to deal with high and volatile metal prices.

Dan Smith – Director, Special Projects